Food from thin air, failure at scale

Biotech works. The business model doesn’t.

Hey —

Quick one today. But sharp.

Here’s the question that’s been stuck in my head:

Why can we turn CO₂ into food — but still can’t make it commercially viable?

You’ve probably seen the headlines about air protein. CO₂ in → microbes → protein out. No cows. No land. No deforestation.

The science works. The bioreactors are running. But the economics? Still broken.

Earlier this month, Austrian biotech Arkeon filed for insolvency. Their pitch was elegant: convert industrial CO₂ into amino acids using extremophile microbes. Clean tech, deep science, real traction.

So why did it collapse?

By all accounts, Arkeon had a real shot.

It had serious tech. A functioning pilot plant. A future-food narrative that matched the climate moment. But this June, it filed for insolvency—another climate moonshot swallowed by the brutal economics of deeptech.

Arkeon’s story isn’t one of overhype or even obvious mismanagement. It’s what happens when a breakthrough arrives just slightly out of sync—with markets, with investors, with reality.

Arkeon was a classic science-forward startup.

Founded in Vienna in 2021 by three researchers—Gregor Tegl, Simon Rittmann, and Günther Bochmann—the company believed it could rewire how humans produce protein.

How? By replacing agriculture with microbes.

Archaea (extremophile microbes) fed on industrial CO₂, not sugar or grain

In return, they secreted all 20 essential amino acids — the foundational building blocks of protein

No cows, no land, no fertilizer runoff

The vision was crisp, radical, and post-agriculture:

“Turn pollution into protein. Feed the world. Skip the cows.”

Unlike a lot of alt-protein startups, Arkeon wasn’t a vibe. It was a lab. By 2023, they’d opened a pilot facility in Vienna, passed EU food safety evaluations, and started shipping early product to partners.

The Tech: Why Gas Fermentation Was (and Still Is) a Moonshot

The idea of turning air into food is no longer fringe. In fact, it’s fast becoming a frontier. As MIT Technology Review put it:

“These companies are creating food out of thin air… Autotrophic microbes fed on carbon dioxide are being grown in vats and dehydrated into protein-rich powders — essentially, edible biomass.”

It’s not just Arkeon. It’s a wave:

Solar Foods (Finland) is producing Solein, a yellow microbial flour made from CO₂ and hydrogen

Air Protein (U.S.) is developing “air chicken” with DARPA funding and a partnership with ADM

NovoNutrients is starting in fishmeal, aiming to move into human protein

All these players are betting on the same idea: Decouple protein from soil, animals, weather, and geography.

But as MIT Tech Review also noted: none of this is commercially viable at scale yet.

Solar Foods’ demo plant, for example, only produces enough Solein to feed every Finn one meal per year.

Arkeon’s process was elegant in theory and proven at small scale:

Input: Captured CO₂, hydrogen, nutrients

Bioreactor: Custom archaea strain secreting amino acids

Output: All 20 amino acids (no animal needed)

End use: Functional ingredients for food manufacturers

This was first-principles biology meeting industrial decarbonization. And critically — it worked. But working isn’t the same as winning.

Why the Food-from-Air Bet Is So Hard to Win

The consumer narrative around microbial protein sounds visionary on stage — but less appetizing on a shelf.

According to a 2024 McKinsey survey of 1,500 U.S. consumers:

50% were open to trying fermented or microbial proteins

Just 28% said they’d try it for health reasons

Taste, trust, and familiarity were the biggest adoption barriers

Terms like bioengineered and fungi-based actively reduced trial intent

Only one phrase reliably worked: “Sustainably made”

That’s a problem — especially for a company like Arkeon, which never sold direct to consumers. Its amino acids were sold B2B — as an ingredient two layers removed from the end buyer.

That made branding nearly impossible, and differentiation almost invisible.

So even if consumers might accept microbial protein in theory, Arkeon had no path to influence that perception directly. They were dependent on a CPG ecosystem still trying to figure out how to message this category at all.

Why Great Tech Isn’t Enough

Even if Arkeon had raised 5× more, it would’ve still faced two steep walls:

A consumer base that doesn’t yet know how to think about microbe-derived food

An ecosystem that hasn’t agreed on what to call it, where to sell it, or how to scale it

The McKinsey data only sharpens the point:

Less than half of consumers were aware of these ingredients

Many rejected products simply because they “didn’t understand how they were made”

Familiar-sounding nutrition claims (“good source of protein”) worked far better than origin claims (“biotech” or “fermented”)

Arkeon wasn’t just trying to scale a complex bio process. It was trying to build a business in a space that lacks category clarity, market standards, and regulatory consistency.

This wasn’t a failure of go-to-market execution. It was a signal: microbial protein — as an industry — is still under construction. And companies betting early need more than tech. They need time, trust, and teams that can build demand scaffolding while engineering the product.

The Money Problem

You can’t scale science with storytelling. You need capital—and the right kind of capital.

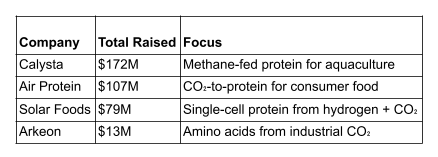

Arkeon raised a modest $13 million in venture funding. Respectable for a SaaS startup. Marginal for industrial biotech. Especially one trying to build a new food system from scratch. To put that in context:

None of these peers had definitively better tech. But they had one of three things Arkeon didn’t:

Earlier momentum

A tighter narrative (DARPA grants, space food, national security)

Or institutional capital (government support, strategic industrial partnerships)

Arkeon had the science, but lacked the external scaffolding that today’s capital-intensive climate companies increasingly need:

Government partnerships

Industrial anchors

Long-horizon, non-VC capital

In that sense, $13M wasn’t just “not enough.” It was the wrong capital structure for a venture environment that had already moved on by 2024.

Why Arkeon Was Always a Tough Bet

Let’s be blunt: this is what a deeptech trap looks like. Brilliant science, commercial purgatory.

1. You need infrastructure, not MVPs

This isn’t code. You can’t test it in Figma. Scaling gas fermentation means bioreactors, purification systems, climate-controlled labs, and years of iteration under strict regulatory regimes.

It’s CapEx-heavy, hardware-dependent, and stubbornly non-linear.

2. The sales cycle is slow and invisible

Arkeon wasn’t selling directly to consumers. It was supplying amino acids to food formulators — who would blend them into ingredients, who would then supply them to brands, who might eventually tell the story to a buyer.

That’s three layers removed from the shelf. There’s no fast loop. No viral GTM. No shortcut to consumer trust.

The companies that survived had a story that moved money:

“Food for Mars” (Air Protein via NASA)

“Protein made in a ditch in Finland” (Solar Foods)

“Replacing fishmeal to save oceans” (Calysta)

What did Arkeon have? “Amino acids from CO₂.” Scientifically accurate. Commercially... difficult.

Storytelling isn’t lipstick — it’s risk translation. If you can’t frame your science in a way that sounds like a market thesis, you’ll get passed over for founders who can.

3. VCs don’t fund science. They fund velocity.

Unless it comes wrapped in a 3-month CAC payback and an AI demo day deck, the market isn’t interested. Arkeon needed infrastructure dollars — project finance, strategic co-investments, blended capital.

What they got was a startup investor base with SaaS instincts.

They were building the right product — but for the wrong market structure.

The Timing Mismatch

On paper, Arkeon had great timing.

It launched in 2021—when climate tech was hot, ESG was mainstream, and plant-based food was still riding the Beyond/Oatly wave.

But over the next 36 months, the ground shifted underneath them.

2022–2023: Global interest rates spiked. Risk capital dried up. Climate investments slowed.

2023–2024: AI took over the narrative. Every LP wanted exposure. Generalist VCs followed.

2024–2025: Climate tech investment dropped 38%. Alt-protein suffered back-to-back double-digit declines.

Meanwhile, microbial food companies—like Solar Foods and Air Protein—were still trying to explain what their product was, let alone how to sell it.

Arkeon ended up holding a high-burn, low-traction business while the market chased OpenAI wrappers and LLM-powered CRM tools.

The Walking Wounded: Sector-Wide Fallout

Arkeon’s collapse wasn’t unique. It’s part of a broader deceleration across foodtech and novel protein.

Over the last 18 months, here’s what’s happened:

Even incumbents aren’t immune:

Beyond Meat posted a 9% sales dip in Q1 and suspended China ops

Beyond Meat Quarterly Revenue Oatly shut its Singapore factory

Market leaders are being squeezed by consumer fatigue, pricing pressure, and supply chain constraints

What we’re seeing isn’t just brand-level weakness. It’s a reckoning with unit economics, capex requirements, and demand signals that never fully materialized.

This was a category built for 2021 valuations—now facing 2025 realities.

Arkeon did almost everything right:

They built a working pilot

Proved the biology

Hit safety milestones

Delivered early product

The Bottom Line

Arkeon didn’t just run out of money.

It ran out of room for error — in a market that stopped forgiving deeptech ambition the moment interest rates rose.

If you're building at the frontier today, the burden isn’t just to invent the future. It’s to align it with the cost of capital, the attention span of your investors, and the fears of your end users.

The science can be perfect. But without the right scaffolding, it won’t matter.